Early spring always feels like a tug‑of‑war between obligation and opportunity. Tax bills come due, tuition deposits loom, and businesses must bulk up inventory for Q2. At the very same time, a new wave of dividend‑rich ex‑dividend dates, four‑week Treasury‑bill auctions, real‑estate crowdfunding drops, and even crypto “spring rallies” tempt investors who crave truly passive profit. Unfortunately, liquidity is usually tied up in long‑term holdings or, worse, saddled with early‑withdrawal penalties.

What if you could tap thousands of dollars quietly locked inside the metal in your driveway without selling any stock, raiding a Roth IRA, or begging a bank for a traditional loan? Auto money title loans provide exactly that bridge, transforming your car, truck, SUV, or motorcycle into fast, short‑term capital you can redirect into high‑yield assets that pay you back while you sleep.

The Auto‑Loan Landscape in Numbers

Before you pledge your title to any lender, it helps to zoom out and understand where auto lending, pricing, and delinquency trends stand right now.

1. Delinquency Rates Are Diverging

- Subprime distress is mounting. As of January 2025, 6.6 percent of subprime auto borrowers were at least 60 days past due, the highest level since the 2008 recession.

- Prime borrowers remain steady. Only 0.39 percent of prime‑score borrowers were 60 days delinquent, up modestly from 0.35 percent a year earlier.

Implication: Traditional banks are tightening their criteria. Borrowers with fair‑to‑poor credit, or those with too much utilization, may find “easy” signature loans or 0‑percent credit cards off‑limits. A collateral‑backed auto money title loan fills that gap because approval hinges on vehicle equity, not FICO scores.

2. Monthly Car Payments Keep Hitting Records

- The average monthly finance payment is on track to reach $731 in March 2025, up $12 from March 2024.

- For new‑car purchases, the Q4 2024 average payment already sat at $742, a hair below the record but still stratospheric.

Implication: Even high earners are feeling payment fatigue. Unlocking dormant equity via a title loan can be the pressure‑release valve, provided you repay on time.

3. Interest Rates Have Plateaued, But at Painful Levels

- The average interest rate on 60‑month new‑car loans sits near 6.82 percent, unchanged year‑over‑year.

- With the Federal Reserve telegraphing a “higher for longer” stance, relief may be slow.

Implication: Banks aren’t likely to slash rates soon. Short‑term title loans maintain their niche: fast approval, independent of macro‑rate swings.

4. Loan Amounts & Vehicle Pricing Continue to Climb

- Americans now borrow an average of $41,572 for new vehicles and $26,468 for used ones.

- The expected average new‑vehicle transaction price in March 2025 is $44,849, up $637 year‑on‑year.

Implication: Vehicle equity, especially for models bought in the pandemic boom, is still substantial. If you own a relatively new car, you may qualify for $10,000–$25,000 in title‑loan proceeds even after depreciation.

5. Tight Credit Meets Opportunistic Investors

Rising delinquencies and high payments create market dislocations, think distressed retail property crowdfunding at a discount, or corporate bonds yielding north of 6 percent. Having liquid cash in March, when many assets are seasonally soft, lets you buy low and reap gains by summer.

Auto Money Title Loans 101 – Mechanics, Math & Misconceptions

What Exactly Is an Auto Money Title Loan?

An auto title loan (aka car title loan or auto money title loan) is a short‑term personal loan, usually 30 day,s secured by the lien on your vehicle’s title. You continue driving, but the lender holds the title as collateral. Fail to repay and they have the legal right to repossess and sell the vehicle to satisfy the debt.

Typical Loan Ranges & LTV

- Loan size: $500 to $50,000

- Advance rate: 25–50 percent of the car’s wholesale (not retail) value

- Term: 30 days is standard; 15‑ and 60‑day contracts exist but are rarer

- Rollovers: Many lenders allow at least one extension, but you must pay a new finance fee each time. Some states cap rollovers at three; others ban them.

Cost Example

Assume you borrow $5,000 for 30 days at a 25 percent finance fee:

- Finance fee: $1,250

- Amount due in 30 days: $6,250

- Effective APR: Roughly 300 percent

At first glance, that’s terrifying, but remember the fee is only in force for a single month. If you channel the $5,000 into a 20‑percent crypto arbitrage, you pocket $1,000 and still owe $250 in net fees. If you dump it into a 4‑week Treasury bill at 5 percent, you earn $21, pay $1,250, and clearly lose. Choosing the right passive‑income vehicle is critical.

Title Loan vs. Personal Loan vs. Credit‑Card Cash Advance

| Feature | Title Loan | Personal Loan | Credit‑Card Cash Advance |

|---|---|---|---|

| Approval Time | Same‑day | 1–7 days | Instant |

| Credit Check | Often none | Yes | Uses card limit |

| Collateral | Vehicle title | None | None |

| Typical APR | 120–300 % | 6–36 % | 24–36 % + fees |

| Loan Term | 15–60 days | 12–60 months | Revolving |

| Max Amount | Up to $50,000 | Up to $100,000 | Card limit |

The trade‑off is speed and simplicity for cost. Used wisely, i.e., for short, high‑return deployments, title loans can be a sharp tool, not a debt trap.

Seasonal Timing & Passive‑Profit Windows

1. Tax Cash‑Flow Crunch

Tax bills land mid‑April, but most people start preparing (and sweating) in March. That liquidity drain sends many investors scrambling for short‑term funding, often dumping dividend stocks just before they pay out. If you can hold your equity positions and use a title loan instead, you may collect that dividend, repay the loan, and keep your principal intact.

2. Real‑Estate Crowdfunding Release Cycles

Platforms such as Fundrise, Arrived, and RealtyMogul frequently roll out new project tranches in March to capture Q2 build schedules. Early investors get preferential shares or higher preferred returns (8–12 percent). Having fast cash on hand means you can claim allocations before they oversubscribe.

3. Four‑Week T‑Bill Auction Arbitrage

The U.S. Treasury holds 4‑week bill auctions weekly. If you draw a title loan for 30 days at a 15 percent finance fee (lower than the example above), and T‑Bills annualize near 5.2 percent, you’ll still lose on the spread so this is not the play. But pair that same 15 percent fee with P2P notes paying 9 percent monthly (yes, they exist on specialized platforms), and suddenly you have a shot.

4. Cryptocurrency “Spring Rally”

Bitcoin halving cycles historically precede spring surges. Short‑term stablecoin staking APYs often spike during liquidity crunches, topping 8–10 percent per month. Again, risk is high, but if you know how to hedge using options or stop‑loss triggers, March can be fertile.

5. Retail & E‑Commerce Inventory Flips

Amazon FBA and Shopify entrepreneurs reorder summer inventory in March to dodge China’s post‑New‑Year bottlenecks. Quick capital to lock in bulk discounts can boost gross margins by 20 percent or more, enough to swamp a 25 percent one‑time finance fee.

Bottom Line: Time your 30‑day title loan so that the asset or activity you fund delivers realized or locked‑in returns within the same window. That’s how you turn a high‑APR instrument into a profitable bridge.

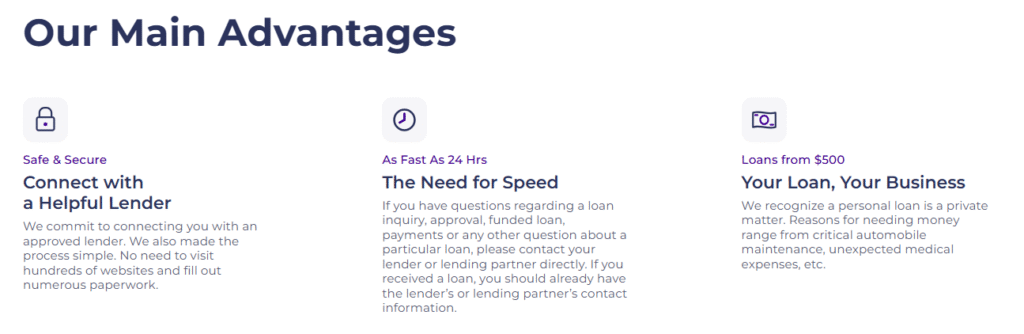

Meet Loans4Title.com – Your Fast Lane to Funding

Most borrowers’ nightmares involve shady storefronts with neon “Easy Cash” signs, borrowing through paychecks, and selling data in dark corners of the web. Loans4Title.com flips that fear on its head by stitching together a network of licensed U.S. lenders accessible through a single, encrypted application.

Speed – Funds in as Little as 24 Hours

Complete the secure online form by 3 p.m. Eastern, and many matched lenders can ACH the funds by the next business morning. That beats waiting a week for a credit union decision, especially when a passive‑income window could close tomorrow.

Safety – Your Data, Locked Down

Fake title‑loan sites love dangling “instant approval” while injecting malware to snatch bank credentials. Loans4Title.com’s SSL encryption and third‑party security badges aren’t window dressing; each badge clicks through to a live verification page.

Convenience – One Form, Many Lenders

Instead of retyping VINs and addresses on six different lender portals, fill out one short form and let the algorithm match you. You’ll get the best available LTV, finance fee, and term combination without cross‑shop headaches.

“I got a loan offer right away without a lot of hassle and I truly appreciate the speedy service.” – Verified borrower review

For readers seeking deeper intel, here’s the quickest route: auto money title loans ↗

From Quick Cash to Passive Profit – Five Tactical Plays That Can Beat the Finance Fee

Everyone’s risk tolerance differs, so consider these as “menu options,” not prescriptions.

1. 4‑Week T‑Bill Ladder + High‑Yield Savings “Booster”

- Estimated net yield: 5.2 percent annualized, or ~0.43 percent for 30 days

- Best for: Ultra‑conservative capital parking

- Reality check: You’ll almost never out‑earn a title‑loan fee, but this combo can serve as a temporary placeholder if your expected cash inflow (bonus, tax refund) arrives before the loan matures.

2. Peer‑to‑Peer Lending Notes (Grade A‑B)

- Estimated net yield: 7–9 percent annualized; some platforms credit interest monthly

- Best for: Diversified income without stock‑market volatility

- Playbook: Filter for 36‑month, low‑risk notes that pay monthly. Allocate your loan proceeds across at least 40 notes to minimize default risk. You’ll capture roughly 0.6–0.75 percent in the first month, enough to dent, though not erase, a 25 percent finance fee. Works better if your fee is below 10 percent, which is feasible for larger, low‑risk vehicles.

3. Dividend Aristocrat ETFs with March Ex‑Dividend Dates

- Estimated dividend yield: 2–3 percent annualized (0.17–0.25 percent monthly)

- Best for: Investors who’d rather own blue‑chip equity than fixed income

- Playbook: Buy an ETF like SCHD or NOBL just before the ex‑dividend date in March; you’ll collect a quarterly payout about three weeks later. Combine with options‑writing (covered calls) to generate extra premium, and you could see 2–4 percent in a single month.

4. Fractional Real‑Estate Crowdfunding

- Estimated yield: 7–12 percent annualized + upside share (quarterly or monthly distributions)

- Best for: Hands‑off landlords

- Playbook: Platforms such as Fundrise often distribute cash every quarter, but some short‑term debt deals (e.g., ground‑up construction mezzanine loans) pay interest monthly. Align your title‑loan maturity with the first interest payment.

5. Crypto Staking & Stablecoin Yields

- Estimated yield: 6–12 percent monthly for risk‑tiered stablecoin pools; 4–10 percent for blue‑chip staking

- Best for: High‑risk appetite and 24/7 monitoring capability

- Playbook: Stake a portion of your loan in a vetted, over‑collateralized stablecoin platform. Hedge downside with protective puts or cash reserves. If yields stay at 8 percent for 30 days, you’ve covered almost a third of a 25 percent finance fee, double that yield, and you’re in profit territory.

Pro Tip: Use a simple spreadsheet: Expected 30‑Day Yield minus Finance Fee equals Net Gain. Don’t borrow if the math goes negative unless you desperately need the liquidity for a non‑financial emergency.

Risk‑Reward Checklist – Stay Profitable & Keep Your Keys

Benefits to Celebrate

- Speed. Capital in a day keeps FOMO away.

- No hard credit pull. Won’t ding your score when mortgage shopping later.

- Leverage. Unlocks equity without selling the underlying asset (your car).

- Control. You choose the passive‑income vehicle instead of letting a bank dictate terms.

Pitfalls to Respect

- High APRs. Even “cheap” title loans can top 120 percent annualized.

- Repossession risk. Default, and goodbye wheels (and possibly your job if commuting).

- Roll‑over spiral. Paying only the fee each month traps many borrowers indefinitely.

- Market risk. The asset you fund could underperform or collapse altogether.

Break‑Even Calculator (DIY)

- Loan amount: $ X

- Finance fee (%): Y

- Fee in dollars: (X × Y)

- Projected 30‑day passive return: Z

- Net: Z − Fee

If Net < 0, reconsider. If Net > 0, proceed, but build a contingency buffer.

Safety Nets & Exit Strategies

- Emergency payoff plan: Have at least 60 percent of the principal parked in a savings buffer or an upcoming paycheck.

- Grace period knowledge: Some states mandate a 10‑ to 15‑day grace period after default. Know yours.

- Straight talk with lenders: Many prefer partial payments over costly repossessions. Negotiate if you hit turbulence.

- Insurance check: Verify your comprehensive coverage; some lenders require it to reduce their risk.

7‑Step Blueprint – How to Tap Capital via Loans4Title.com

Time required: As little as 15 minutes for the form, 24 hours to funding

| Step | Action | Outcome |

|---|---|---|

| 1 | Fill the secure online form (name, address, SSN, income, vehicle year/make/model/VIN) | Receive ACH deposit – often the next business morning |

| 2 | See the tentative loan amount & fee | An instant preliminary decision appears on the screen |

| 3 | Vehicle inspection – upload geo‑tagged photos or schedule a drive‑by | Confirms value & condition |

| 4 | E‑sign digital loan agreement | Locks in terms, no in‑person paperwork |

| 5 | Upload supporting docs (title, insurance, ID, proof of address/income) | Lender performs final verification |

| 6 | Funds hit the checking account | Funds hit checking account |

| 7 | Repay in 30 days (or renew responsibly) | Lien released, title returned |

Pro move: Synchronize Step 6 with the passive‑income asset’s purchase window, e.g., an ETF buy before ex‑dividend or a crowdfunding funding round.

FAQs – Auto Money Title Loans

Q1: Can I qualify if my car isn’t fully paid off?

Yes, if the remaining lien is small enough that you still possess sufficient equity. The new lender may refinance the existing payoff and issue a smaller net advance to you.

Q2: What credit score do I need?

Often none. Many Loans4Title.com‑network lenders rely solely on collateral value and income verification.

Q3: How many rollovers are legal in my state?

Varies wildly: some states (e.g., Arizona) cap at five, others (e.g., Georgia) at zero. Consult your state’s Department of Financial Institutions website or ask the lender directly.

Q4: Will applying hurt my FICO?

Most lenders perform a soft pull. A hard inquiry may occur if they need extra validation, but this is rare and typically costs fewer than five points.

Q5: How soon can I re‑borrow after payoff?

Immediately, provided you still meet equity and income criteria. However, churn borrowing defeats the passive‑income goals; focus on one profitable cycle at a time.

Q6: What happens if I’m late by a day or two?

Late fees accrue, and interest (or additional finance charges) may compound daily. Communicate early; many lenders offer a short grace period or partial payment plan.

Conclusion – Drive Your Passive Profit Forward

March 2025 is shaping up as a perfect storm of financial pressure and investment opportunity. Rising car payments squeeze wallets, yet market dislocations from real‑estate debt to dividend blue chips beckon investors with higher yields than we’ve seen in years. Auto money title loans unlock the liquidity you need now, without liquidating long‑term assets or jumping through bank‑loan hoops.

Used recklessly, a high‑APR title loan can torch your finances and cost you your car. Used strategically paired with disciplined passive‑income plays that mature inside 30 days, it can be a powerful bridge that amplifies returns and accelerates wealth‑building.

The key is speed, security, and transparency. Loans4Title.com delivers all three through a single, encrypted form that can fund you as soon as tomorrow morning.

Need capital by tomorrow to seize a once-in-a-lifetime passive‑income deal?

👉 Apply for auto money title loans at Loans4Title.com now – get funded fast, grow profits faster!

Fill out the 60‑second form, receive an instant match, and turn your car’s idle equity into the springboard for your next wealth milestone.