Most people consider personal loans to cover unexpected expenses or consolidate debt, but understanding your varied loan options helps you choose the best fit for your financial goals. You’ll encounter loans with different terms, interest rates, and fees, some offering fast online approval, while others require collateral or come with high APRs that can quickly escalate your debt. By evaluating these factors carefully, you can secure funding that supports your needs without risking your credit or financial stability.

>>>>>>>>>Get Your Free Personalized Loan Quote<<<<<<<<<<<<

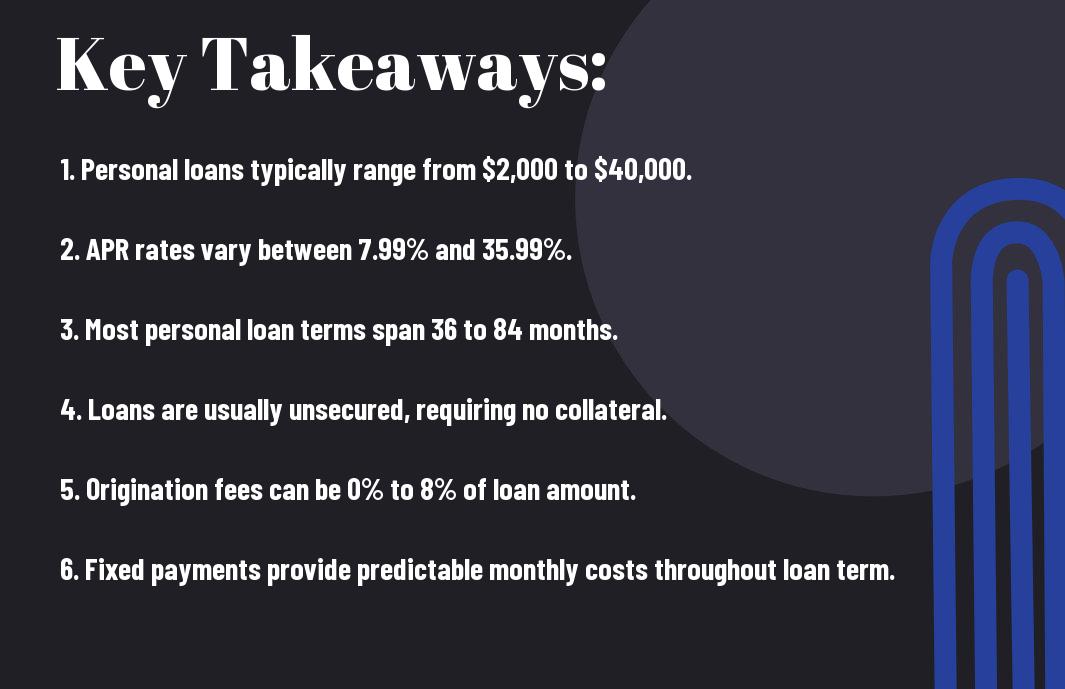

Key Takeaways:

- Online personal loans typically range from $2,000 to $40,000, with some lenders offering up to $100,000, and repayment terms commonly between 36 and 84 months.

- Interest rates (APR) vary widely from about 7.99% to 35.99%, often accompanied by origination fees ranging from 0% to 8%, which affect the total borrowing cost.

- These loans are generally unsecured, meaning no collateral is required, and the loan pricing depends on credit factors like FICO score, debt-to-income ratio, and cash-flow stability.

- The digital application process includes soft and hard credit pulls, identity verification, income checks, and ACH disbursement for fast funding.

- Instant approval usually refers to immediate pre-qualification or conditional offers, while actual funding can take from the same day up to 24 hours, depending on the lender’s ACH processes.

Types of Loan Options

A variety of personal loan options exist to suit your financial needs. These include:

- Secured Loans backed by collateral.

- Unsecured Loans without collateral requirements.

- Installment Loans with fixed monthly payments.

- Payday Loans are short-term, high-interest emergency cash.

- Peer-to-Peer Loans are funded by individual investors online.

After exploring these types, you can choose the best that fits your budget and goals.

| Loan Type | Description |

|---|---|

| Secured Loans | Require collateral like a house or car to secure the loan. |

| Unsecured Loans | No collateral needed; based mainly on your creditworthiness. |

| Installment Loans | Repaid over time in fixed monthly payments. |

| Payday Loans | Short-term, small-dollar loans with very high APRs. |

| Peer-to-Peer Loans | Loans are funded by individuals through online platforms. |

Secured Loans

About secured loans, you use an asset like your home or vehicle as collateral, which often helps you secure lower interest rates and higher loan amounts. However, if you miss payments, you risk repossession of the asset. These loans typically offer longer repayment terms, making monthly payments more manageable.

Unsecured Loans

For unsecured loans, you don’t need to pledge collateral, making approval faster and less risky for your assets. Interest rates can be higher since lenders rely on your credit score and income verification. Terms usually range from 36 to 84 months, with fixed payments that make budgeting easier.

Options for unsecured loans are flexible, especially with online lenders offering instant approval and same-day funding. While you avoid collateral risk, be aware that APR rates can be higher, often between 7.99% and 35.99%, so you should carefully compare offers and factor in origination fees. Missing payments directly impacts your credit score, making timely repayment vital. On the positive side, these loans are ideal for quick access to cash for investments or debt consolidation without risking your home or car.

Personal Loans

There’s a variety of personal loan options designed to fit your financial needs, offering flexible amounts and terms. These loans often range from $2,000 to $40,000, with repayment terms spanning 36 to 84 months and APRs between 7.99% and 35.99%. Whether for debt consolidation or funding a project, personal loans provide fixed monthly payments, helping you plan your budget effectively while giving you access to fast funding options.

>>>>>>>>>Compare Top Loan Offers Now<<<<<<<<<<<<

Standard Personal Loans

Loans from traditional lenders typically offer fixed rates and terms, allowing you to borrow between $2,000 and $40,000 with repayments spread over three to seven years. These loans are unsecured, meaning you won’t risk collateral like your home or car, though your credit score will influence your APR, which can range up to 35.99%. Fixed payments make managing your budget easier, and digital application processes can deliver funding within 24 hours, helping you seize timely investment opportunities.

Peer-to-Peer Lending

Between individual investors and you, peer-to-peer lending platforms connect borrowers with private lenders, often providing competitive rates and faster access to funds. This alternative removes traditional banks from the equation, sometimes enabling you to secure loans that align better with your credit profile and funding timeline.

The peer-to-peer lending model offers you the advantage of potentially lower interest rates and quicker approval compared to banks, as loans are funded by multiple individual investors through an online platform. However, your loan still depends on your creditworthiness, and defaults can negatively impact your credit. While these loans are unsecured, meaning you won’t risk collateral, you should be aware of possible higher APRs for lower credit scores and review origination fees carefully. The fully digital application accelerates the process, but it’s important to stay disciplined with repayments to protect your credit and maximize the benefits.

Mortgage Loans

Not all personal loans suit mortgage purposes, but mortgage loans specifically help you purchase or refinance real estate with sizable funds and extended terms. These loans often have lower interest rates than personal loans because they are secured by your home, allowing you to leverage real estate as an asset. Choosing the right mortgage type affects your monthly payments and long-term financial flexibility, so understanding options like fixed-rate and adjustable-rate mortgages empowers you to make informed choices aligned with your goals.

Fixed-Rate Mortgages

Before committing, know that Fixed-Rate Mortgages lock your interest rate for the entire term, often 15 to 30 years, providing predictable monthly payments. This stability helps you budget effectively, especially when interest rates are low. Fixed rates mean your loan payment won’t rise, shielding you from market fluctuations. However, you might pay slightly higher rates compared to adjustable loans initially, so weigh your appetite for risk against the benefit of payment certainty when you plan your home financing.

Adjustable-Rate Mortgages

Among your mortgage alternatives, Adjustable-Rate Mortgages (ARMs) start with lower initial rates than fixed loans, which can boost your cash flow early on. These loans adjust periodically, often after a fixed introductory period based on market interest rates, meaning payments may fluctuate. If you expect to sell or refinance before rate resets, ARMs can save you money, but you must be prepared for possible payment increases when rates rise.

Fixed-rate mortgages offer you stability by keeping your interest rate constant throughout the loan term, which means your monthly payments remain predictable regardless of market changes. This makes budgeting easier and reduces financial stress. In contrast, Adjustable-Rate Mortgages start with lower rates but come with the risk of payment increases as interest rates adjust, potentially doubling your monthly obligation. Using an ARM can increase your financial risk over time, especially if interest rates climb significantly. However, ARMs can be beneficial if you plan to move or refinance before adjustments begin, giving you lower initial costs. Understanding these dynamics helps you align your mortgage choice with your financial situation and goals.

Business Loans

Despite the growing popularity of fast personal loans, business loans remain a common choice if you want to fund growth or startup costs. These loans typically offer larger amounts and longer terms, giving you more flexibility. However, securing traditional business loans can take time, sometimes weeks, potentially causing you to miss timely opportunities. Exploring all available options, including faster, alternative financing, helps you deploy capital when it matters most to build your business efficiently.

Traditional Business Loans

Against the backdrop of quicker online funding, traditional business loans often require thorough paperwork, strong credit, and collateral. Approval times can stretch from days to weeks, which may slow your ability to act on fast-moving deals. While interest rates may be lower, you should weigh the waiting period and rigid qualification criteria before choosing this route for your business financing needs.

Alternative Financing Options

By turning to alternative financing, like instant-approval personal loans or fintech platforms, you can access funds in hours rather than weeks. These options often have higher APRs (from 7.99% to 35.99%) and smaller loan sizes but offer the speed and flexibility that help you seize timely market opportunities and grow your cash-flow assets with less delay.

A wide range of alternative financing options has emerged to meet your need for speed and convenience. While the fixed-rate terms and unsecured structure of online personal loans protect your assets from repossession, the higher interest rates and origination fees mean you must carefully calculate your passive-profit spread to ensure your investments generate more than your loan costs. Leveraging a platform like GetCash4Me can help you compare multiple lenders instantly, boosting your chances of securing favorable terms and same-day funding to capitalize on growth opportunities without losing time.

Student Loans

Your path to funding education often includes choosing between federal and private student loans. Understanding the differences helps you select the best option tailored to your financial situation. While both aim to support your studies, they vary significantly in interest rates, repayment terms, and eligibility requirements.

Federal Student Loans

With federal student loans, you benefit from government-backed options featuring fixed low interest rates and flexible repayment plans. These loans usually offer income-driven repayment and possible loan forgiveness, making them a safer choice during your schooling and beyond.

Private Student Loans

After exhausting federal options, you might consider private student loans, which are offered by banks and credit unions. These loans often come with higher interest rates and less flexible repayment terms, so you need to compare offers carefully, considering fees and your credit profile.

To navigate private student loans effectively, understand that these are unsecured loans with rates ranging broadly, often between 7.99% to 35.99% APR, depending on your creditworthiness. Unlike federal loans, private lenders usually require a good credit score or a cosigner. Origination fees can reach up to 8%, impacting your total cost. You should also be cautious of fixed versus variable rates and make sure the loan payments fit your projected income during repayment to avoid financial strain.

Auto Loans

Now, when you need to finance a vehicle, auto loans offer tailored solutions for both new and used cars. These loans typically range from a few thousand to $100,000, with repayment terms varying between 24 and 84 months. By securing a loan with competitive APRs often between 7.99% and 35.99% you can spread the cost of your vehicle over time while managing monthly payments that fit your budget and financial goals.

New Car Loans

After deciding on a new car, you can leverage new car loans designed with longer terms and potentially lower interest rates compared to used car financing. These loans often incorporate dealership incentives and special APR offers, helping you secure affordable payments and maintain predictable budgeting for your new vehicle investment.

Used Car Financing

Financing a used car usually involves higher APRs and stricter loan terms compared to new car financing. You can expect rates from 8% upward, influenced by the car’s age, condition, and your credit profile. It’s important to match your loan term to your expected ownership period and monthly cash flow, ensuring the payments remain manageable.

Used car financing requires careful evaluation since interest rates tend to be higher and loan terms shorter, increasing monthly costs. Since these loans are almost always unsecured, you won’t risk your vehicle being repossessed for missed payments, but late or missed payments can quickly damage your credit. To protect your investment, focus on securing a fixed-rate loan with a realistic monthly payment that your budget can cover, even if unexpected expenses arise.

Final Words

As a reminder, personal loan options offer you flexible, fast funding solutions that can accelerate your investment opportunities when timed right. By carefully choosing loans with competitive APRs, manageable terms, and aligning payments with your asset’s cash flow, you gain financial leverage without risking collateral. Using online platforms can simplify the process and speed up access to capital, allowing you to act swiftly in dynamic markets. Ultimately, your disciplined approach to borrowing and reinvesting will determine how effectively these loans contribute to your long-term passive income goals.

FAQ

Q: What types of personal loans are commonly available online?

A: Online personal loans typically range from unsecured installment loans to lines of credit. Common loans have amounts between $2,000 and $40,000, with repayment terms from 36 to 84 months. Interest rates vary widely, generally between 7.99% and 35.99% APR, depending on creditworthiness and lender. Some lenders also offer no-origination-fee options or loans with quick disbursement times, ideal for fast funding needs.

Q: How does loan approval impact my credit score during the application process?

A: The application process usually includes multiple credit inquiries with different impacts. A soft pull during pre-qualification does not affect your credit score or appear on your report. However, once you submit a formal application, a hard credit pull occurs, which might cause a 3–5 point temporary dip. Responsible repayment of the loan can build credit over time by showing on-time payments.

Q: What should I consider when comparing APR and origination fees on personal loans?

A: When evaluating loan offers, consider both the APR and any origination fees, as fees can significantly affect the total cost of the loan. Sometimes, a loan with a slightly higher APR but no origination fee may be less expensive overall compared to a lower APR loan with a sizable upfront fee. Review the loan’s Truth-in-Lending Disclosure for complete cost details before making a decision.

Q: Are online personal loans secured or unsecured, and what does that mean for borrowers?

A: Most online personal loans are unsecured, which means you don’t have to provide collateral like a house or car. This reduces the risk of losing assets if you miss payments, but loans are priced based on credit score, income, and debt-to-income ratios. Failure to repay can harm your credit and lead to collections, but your property cannot be repossessed under an unsecured loan.

Q: How can I best match a personal loan’s repayment terms with my investment cash flow?

A: To maintain positive cash flow, align your loan payments with the income generated by the asset you’re funding. Aim for loan payments that use no more than 60% of your average monthly net returns to provide a buffer for seasonal fluctuations or unexpected expenses. Choosing fixed-rate loans with manageable monthly payments helps protect against interest rate volatility and ensures that your asset’s income consistently covers debt service.

>>>>>>>>>Find the Lowest Rates Today<<<<<<<<<<<<