You’ve spent years dutifully feeding a 401(k) or Traditional IRA, hoping compound interest and market averages will carry you through retirement. Yet recent headlines hint at a bumpier road ahead: elevated stock valuations, stubborn inflation, and bond yields struggling to outrun living costs. Little wonder the phrase “passive profit in crypto” keeps popping up in finance podcasts.

Still, most disciplined savers hesitate to dive into Bitcoin on a whim. They want the upside but without sacrificing the tax perks or the regulatory peace of mind they’ve enjoyed with conventional retirement vehicles. Enter the self‑directed Bitcoin IRA, an IRS‑recognized account that wraps Bitcoin’s growth potential inside the familiar structure of a Traditional or Roth IRA.

But where do you start? Custodianship rules, cold‑storage security, transfer paperwork each can feel like a minefield. That’s why a free consultation with a specialist isn’t a nice-to-have; it’s essential. Over the next several sections, you’ll see exactly how talking with a BitIRA Digital Currency Specialist can transform confusion into clarity, before you move a cent of your nest egg.

>>>>>>>>>>>>>>Get Your Free Bitcoin IRA Consultation Now<<<<<<<<<<<<<<<<

Bitcoin IRA 101

A Bitcoin IRA is a self‑directed individual retirement account that lets you purchase, hold, and sell Bitcoin (and often other cryptocurrencies) inside the same tax shelter you’d use for stocks or mutual funds. The IRS already allows alternative assets such as gold bullion and real estate in IRAs; Bitcoin simply joins that list.

- Traditional Bitcoin IRA: Contributions may be tax‑deductible today; withdrawals are taxed as ordinary income in retirement.

- Roth Bitcoin IRA: You contribute after‑tax dollars now but enjoy tax‑free withdrawals of both principal and potential crypto gains later.

Either path means your crypto’s day‑to‑day price swings don’t trigger annual capital‑gains taxes crucial for long‑term compounding.

Three Built‑In Advantages for Long‑Term Wealth‑Builders

Long‑Term Growth Potential

Since its launch in 2009, Bitcoin has advanced from fractions of a cent to tens of thousands of dollars per coin. Yes, volatility is real, but so is the long‑term trajectory. For passive investors seeking an asymmetric upside, allocating even a modest percentage of their retirement funds to Bitcoin can meaningfully tilt future returns.

Shelter from Overvalued Equities

When Goldman Sachs warns that stocks appear “elevated on almost every metric,” it signals that diversification away from traditional equities isn’t alarmist, it’s prudent. Bitcoin’s supply cap and decentralized nature give it different drivers than corporate earnings or central‑bank policy, providing a hedge against possible equity‑market pullbacks.

Tax‑Deferred (or Tax‑Free) Compounding

Trading Bitcoin in a taxable brokerage account can be an administrative headache; every rebalance becomes a reportable event. Inside a Bitcoin IRA, however, gains roll over untaxed until distribution (Traditional) or forever (Roth). Imagine harvesting a decade of potential crypto appreciation without annual IRS friction.

The Value of a Free Consultation Before You Commit a Dollar

You wouldn’t buy a rental property sight unseen. Likewise, you shouldn’t fund a crypto IRA without understanding:

- Custody mechanics: Who holds the keys, and how are they protected?

- Fee structure: Setup charges, annual custodian fees, and any trading spreads.

- Rollover logistics: How to move assets from a current 401(k) or IRA without a taxable distribution.

- Asset menu & liquidity: Which coins are available, and how quickly can you trade or rebalance?

- Exit strategy: The rules for taking distributions at retirement age or earlier, if life throws surprises.

A no‑cost, no‑obligation call lets you probe these points with a licensed specialist, sidestepping hours in Reddit rabbit holes. If the numbers or security model don’t impress you, simply walk away your wallet and peace of mind intact.

Curious whether a Bitcoin IRA suits your timeline and risk tolerance? Schedule a free consultation with BitIRA to get personalized answers in 15 minutes.

Meet BitIRA A Quiet Pioneer in Crypto Retirement Accounts

Founded in 2017 as a subsidiary of Birch Gold Group, BitIRA focuses exclusively on Digital IRAs. Over the years, it has earned a reputation for balancing robust security with approachable customer service a blend prized by passive investors who prefer “easy button” solutions.

Snapshot of BitIRA’s Offering

| Feature | How It Benefits Passive Investors |

|---|---|

| Military‑Grade Cold Storage | Assets remain offline, insulated from hacks and exchange failures. |

| Multi‑Key Encryption | Even internal staff can’t move funds unilaterally reduces single‑point risk. |

| Fully Insured Vaults | All‑risk policy covers theft, damage, and natural disasters. |

| Low $1,000 Minimum | Accessible entry point; scale at your own pace. |

| Institutional‑Grade Liquidity | Trades executed through premier exchange partners for tight pricing. |

| IRS‑Compliant Custodians | Equity Trust Co. and others handle reporting, so tax season stays simple. |

BitIRA supports a curated list of major cryptocurrencies, Bitcoin, Ethereum, Litecoin, Stellar Lumens, Bitcoin Cash, and Ethereum Classic, so you can diversify while avoiding obscure tokens that add complexity without proven track records.

What Happens on a BitIRA Free Consultation Call?

Below is a first-hand walk‑through so you know what to expect, from initial hello to a fully funded account.

Step 1: Schedule & Intro Chat

You book a slot online or call 800‑299‑1567. At the appointed time, a Digital Currency Specialist asks about your retirement goals, risk comfort, and existing tax‑advantaged accounts. Expect clear explanations in plain English no jargon barrage.

Step 2: Paperwork Guidance

If a Bitcoin IRA feels right, the specialist drafts your self‑directed IRA application with a trusted custodian (currently Equity Trust or Preferred Trust). You review, e‑sign, and upload IDs. BitIRA coordinates the rest.

Step 3: Funding Your Account

You can roll over all or part of a Traditional, Roth, SEP, or SIMPLE IRA and most 401(k)s from previous employers without triggering a taxable event. Prefer fresh capital? Annual contribution limits apply ($7,000 if under 50; $8,000 if 50+ for 2025). BitIRA’s team handles the transfer logistics, so funds land in the new IRA, not in your personal bank account (avoiding withholding headaches).

Step 4: Asset Selection & Purchase

Once cash hits the IRA, you receive real‑time quotes for Bitcoin or other supported coins. Confirm your allocations; BitIRA executes trades with its liquidity partner (Genesis or equivalent). Settlement is typically instant.

Step 5: Cold‑Storage Transfer & Confirmation

Purchased crypto is whisked into true cold storage, secured by multi‑signature hardware modules separated in geographically distant vaults. You receive transaction IDs and a dashboard login to view balances 24/7.

Step 6: Ongoing Support

Your specialist remains on call for:

- Additional contributions or rollovers

- Rebalancing into new coins as BitIRA expands its list

- Required Minimum Distributions (RMDs) if applicable

- Early‑distribution scenarios (disability, first‑home purchase, etc.)

Thinking this step‑by‑step help could simplify your life?

→ Lock in your no‑obligation BitIRA call now

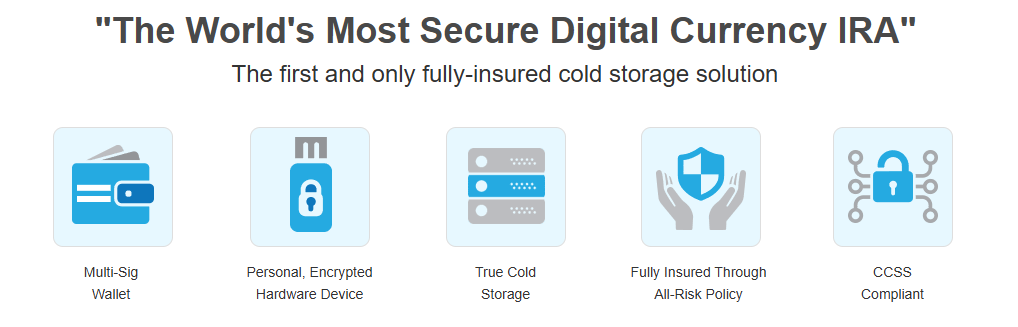

Security You Don’t Have to Babysit

Passive investors value peace of mind as much as returns. BitIRA stacks multiple protections to deliver exactly that.

- True Cold Storage

Coins are stored offline, air‑gapped from the internet, not just in “cold wallets” sitting in a data center closet. - Multi‑Signature Architecture

Moving funds requires several private‑key fragments held by independent parties. No single insider, thief, or even a rogue nation‑state can drain wallets unilaterally. - Personal Encrypted Hardware Device

For certain account tiers, BitIRA issues a hardware device that lets you verify balances without ever exposing keys online. - CCSS Level 3 Compliance

The CryptoCurrency Security Standard (CCSS) is to digital assets what SOC 2 is to cloud services. Level 3, its highest tier, demands robust segregation of duties and penetration testing. - All‑Risk Insurance

Policies underwritten by Lloyd’s of London cover not just cyber‑theft but also “acts of God,” adding another sleep‑well layer.

Transparent Fees, Minimums & Typical Timelines

| Cost Category | Amount | Notes |

|---|---|---|

| Account Minimum | $1,000 | Can be rolled over or newly contributed. |

| One‑Time Setup Fee | $50 | Covers custodian paperwork. |

| Annual Custodian Fee | $300–$1,000 | Tiered by account balance. |

| Trading Commission | $0 | BitIRA makes a spread inside quoted price; no separate line item. |

Timeline Snapshot

- Consultation to paperwork: Same day in most cases.

- Transfer/rollover clearing: 3–14 business days (depends on releasing custodian).

- Purchase & cold‑storage settlement: Minutes once funds clear.

That means you could go from “curious phone call” to “Bitcoin safely inside an IRA” within two to three weeks, often faster for direct contributions.

Expert Endorsements & Market Credibility

“Bitcoin is better than currency in that you don’t have to be physically in the same place and, of course, for large transactions, currency can get pretty inconvenient.” Bill Gates, Microsoft Founder

“I have invested in Bitcoin because I believe in its potential; the capacity it has to transform global payments is very exciting.”

Sir Richard Branson, Virgin Group Founder

BitIRA itself has appeared in Bloomberg, CNBC, MarketWatch, and other mainstream outlets, often cited for its rigorous security model. While media logos won’t guarantee returns, they signal a level of due diligence that fringe crypto startups rarely achieve.

Rapid‑Fire FAQ

Q: Is a Bitcoin IRA legal with the IRS?

Yes. The IRS allows “alternative assets” in self‑directed IRAs, provided you use a qualified custodian who reports transactions and valuations annually.

Q: Can I keep my existing 401(k) separate?

Absolutely. A rollover is optional you can move as little or as much as you wish, or simply open a new Roth IRA alongside your 401(k).

Q: What if Bitcoin’s price crashes?

Market risk never disappears. Inside an IRA, however, you retain the tax benefits, and you can rebalance into other assets if your long‑term thesis changes.

Q: Am I locked into BitIRA forever?

No. You can transfer funds to another custodian or back to a conventional brokerage IRA at any time. Standard custodian transfer fees may apply.

Q: How soon can I access my crypto?

Standard IRA rules apply: age 59½ for penalty‑free withdrawals (Roth IRAs allow contribution withdrawals anytime). Hardship or first‑home exceptions still stand.

Next Steps: Claim Your Free Consultation

A Bitcoin IRA offers a compelling trio: security, tax optimization, and potentially explosive upside. Yet its real power lies in aligning with your risk tolerance, retirement horizon, and existing portfolio. The smartest way to make that call is to talk with a specialist who’s walked thousands of investors through the process.

Prefer the phone? Call 800‑299‑1567.

Final Thought

Diversification isn’t about predicting the future; it’s about preparing for multiple futures. A carefully structured Bitcoin IRA set up with the guidance of a seasoned specialist could be the bridge between the world you know and the financial frontier you don’t want to miss. The consultation is free; the insight may prove priceless.

>>>>>>>>>>>>>>Download our Free Bitcoin IRA Guide<<<<<<<<<<<<<<<<

FTC Disclaimer and Disclosure

This article is intended for informational purposes only and should not be considered investment advice. The content is based on publicly available information and is not a solicitation to buy or sell any financial products. Any investment decisions should be made after consulting with a financial advisor.